Mauricio Junior

Mauricio Junior

Can I move my 401k from my old company to my new 401k?

Yes — in most cases you can...

Yes — in most cases you can move your old 401(k) into your new employer’s 401(k), and this is called a 401(k) rollover.

Your main options

When you leave a job, y ...

Subscribe easy2invest.org

Make your money work for you. Articles, videos, shorts, ebooks, books, forum, community and more.

You can cancel anytime.

Log In

Subscribe now

All information in this article is not a recommendation.

We show examples, and you need to analyze.

We are not responsible for your decisions and investments.

Related articles

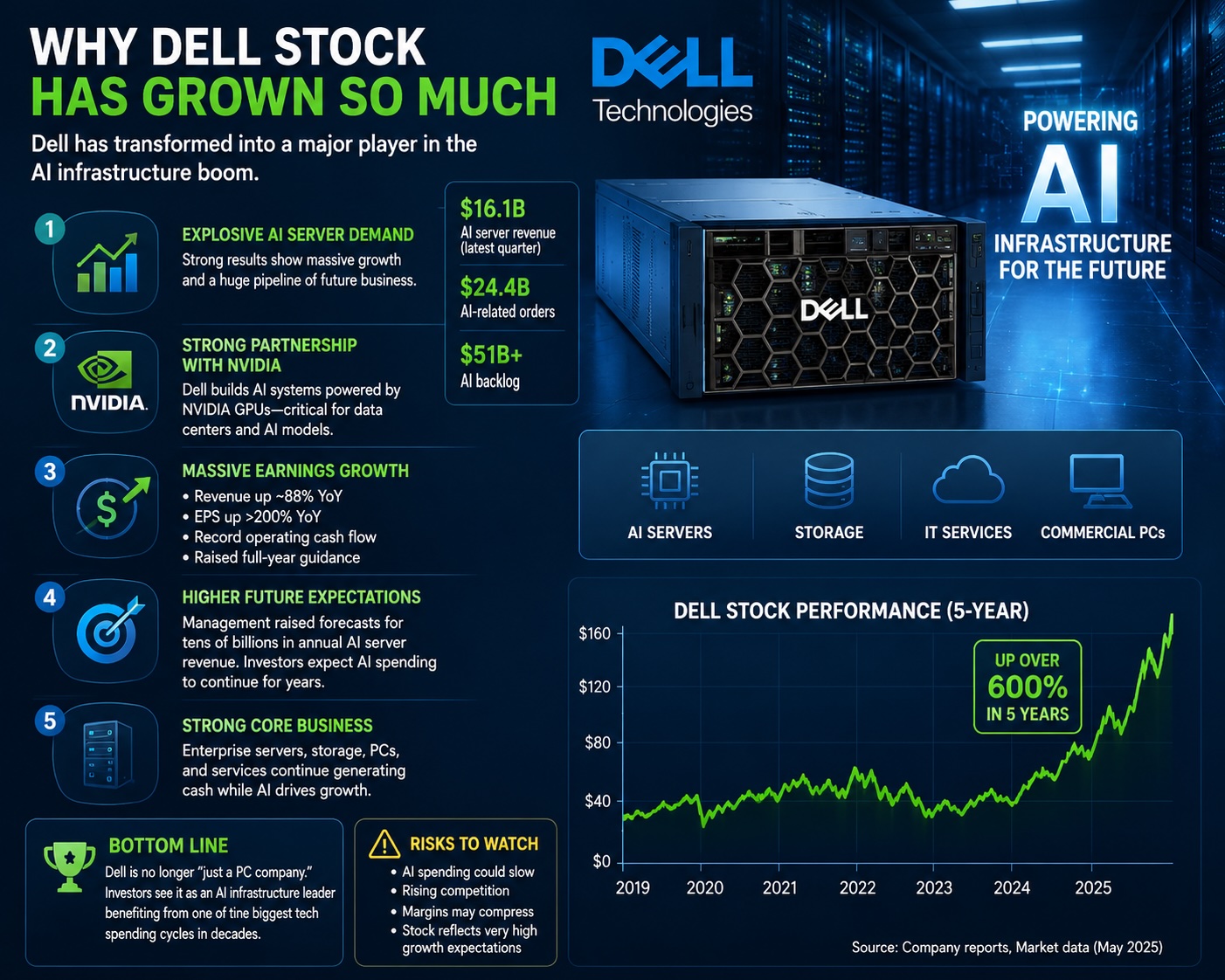

Why has DELL stock grown so much?

The biggest reason Dell stock has surged is simple

What is the risk of letting AI do trader investments?

Letting AI handle trading or investing can be p...

How to manage your money?

Managing money well is less about being “rich”...

How to RETIRE by 30?

Retiring by 30 is possible, but it usually...

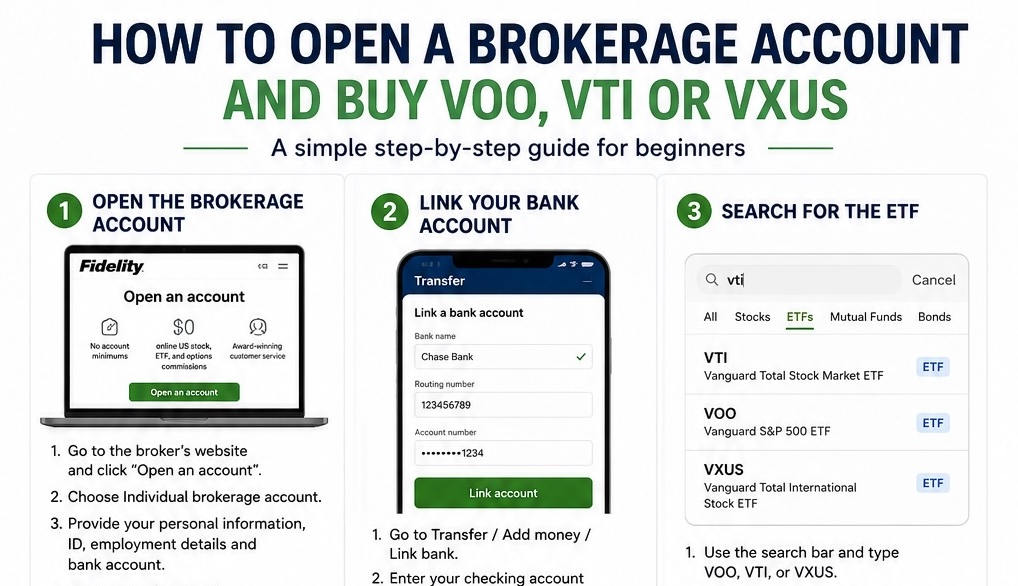

How can I begin start investing with just $50?

Follow the steps showing the simple way to do it

From $20 a day to a millionaire

Everything consistent in our lives is not comin...

Investing My First $100: A Simple Beginner’s Strategy

Starting your investment journey doesn’t require t

VXUS (Vanguard Total International Stock Index Fund) ETF

The most popular international index fund...

I requested the A.I. to generate a portfolio for investment using $10,000

I wouldn’t try to “outsmart” the market

How to build my first portfolio?

Building your first investment portfolio doesn’t..