Mauricio Junior

Mauricio Junior

Tax Optimization Strategies

Do you know about this strategies

Since you're a W-2 employee, your wife is 1099 (self-employed), and you have 2 kids + a dependent mother-in-law, you actually have some very strong tax opt ...

Subscribe easy2invest.org

Make your money work for you. Articles, videos, shorts, ebooks, books, forum, community and more.

You can cancel anytime.

Log In

Subscribe now

All information in this article is not a recommendation.

We show examples, and you need to analyze.

We are not responsible for your decisions and investments.

Related articles

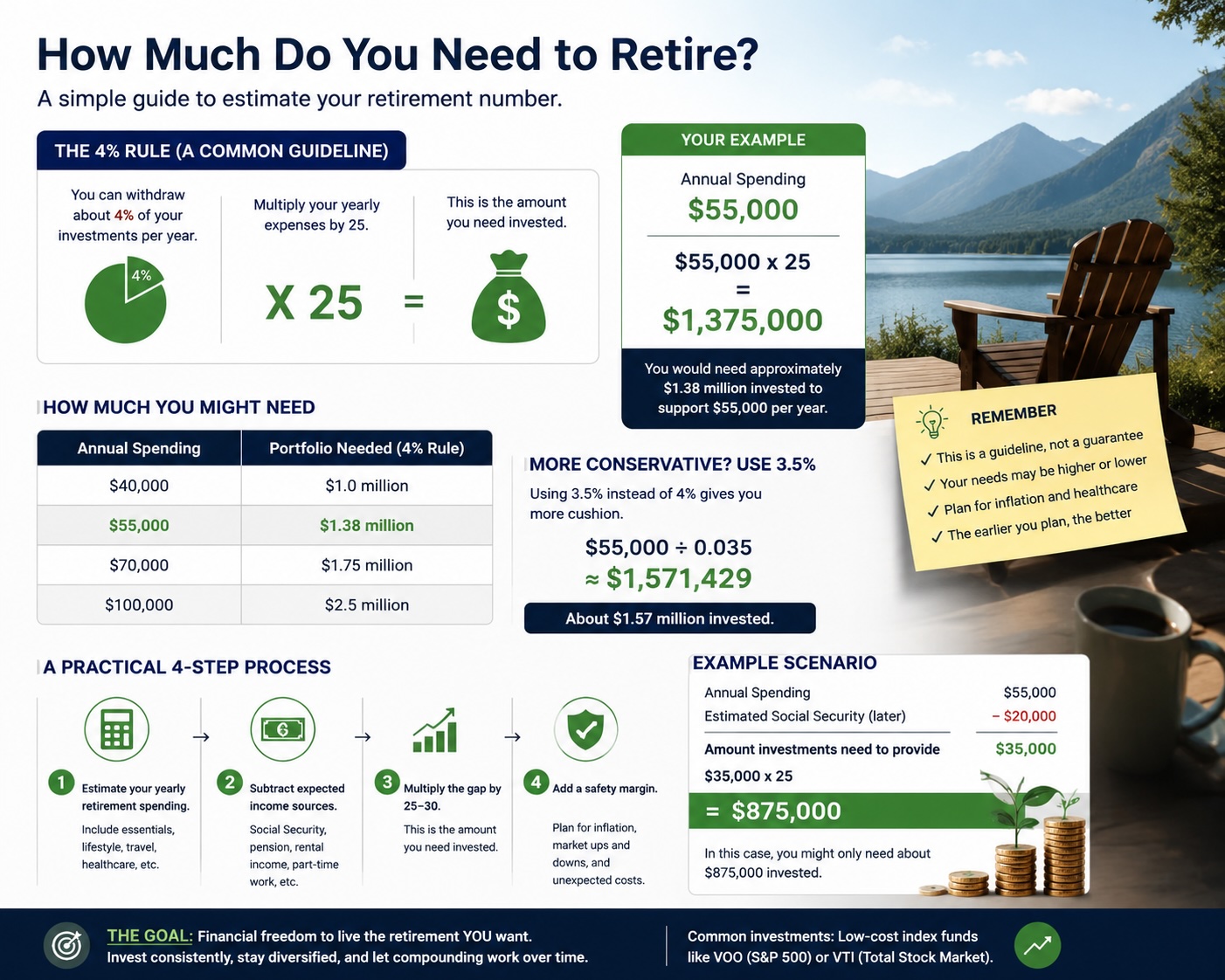

How do I figure out how much I'll need to retire?

Start with the first step, how much you...

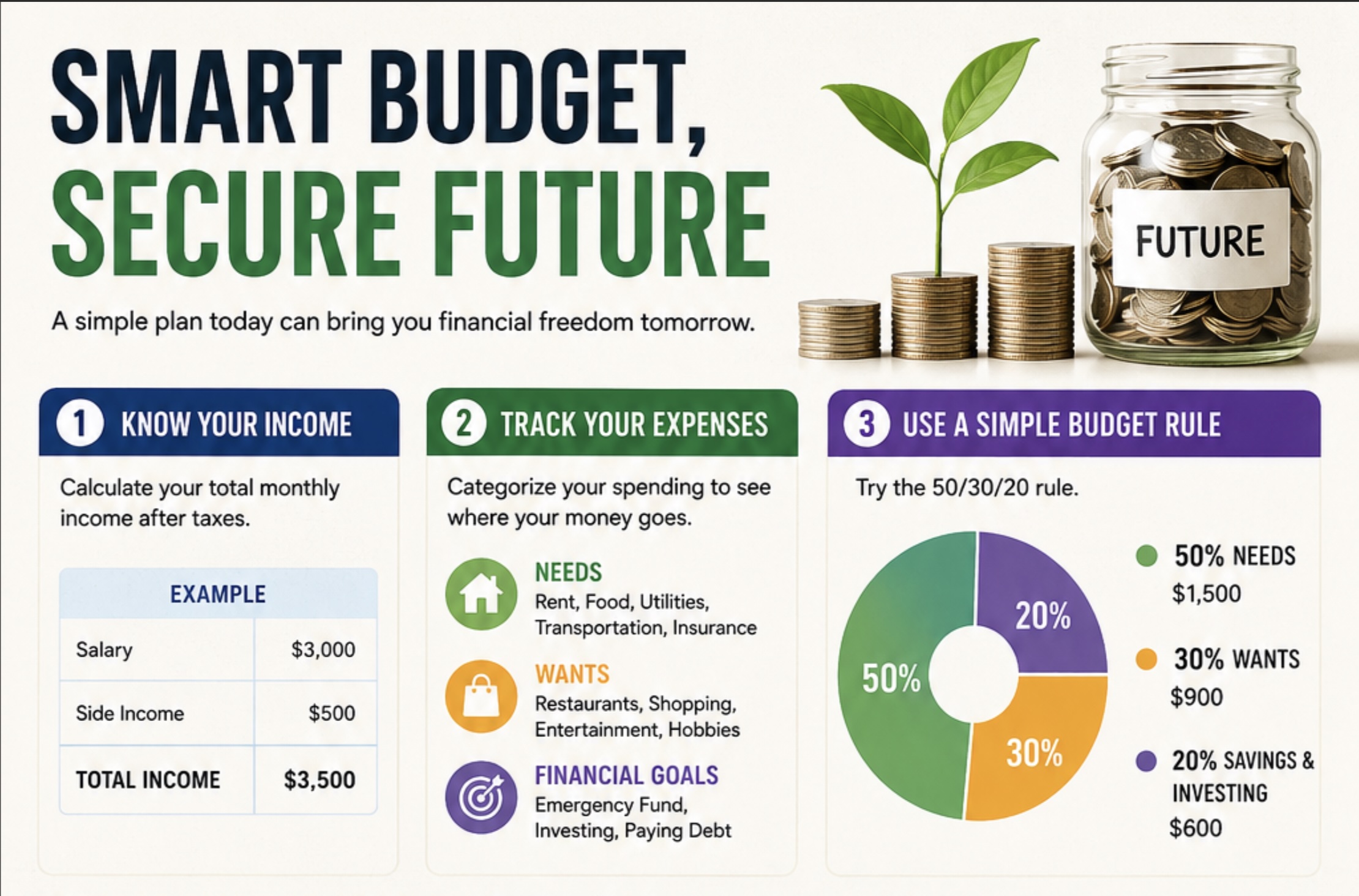

How to deal with the finance budget?

Managing your finances is about controlling ...

MSTR Bitcoin

MSTR is the stock of Strategy...

When is it a good time to buy Bitcoin?

There’s no “perfect” moment to buy Bitcoin but...

What is the best broker to use now, based on trust?

Check here the best brokers to use

Smart Budget Tracker

How to control it?

Rules about IRA Individual Retirement Account

Step by step with examples

I’m 1099 and I would like to optimize my tax

What to do in my case?

How much do I need to invest in KO to get $1000 from dividends?

Check all the calculations

Where else can I save my money better than in a bank savings account?

Better than savings account