Mauricio Junior

Mauricio Junior

REIT Simon Property Group (SGP) paying between 4.5% and 4.7% of dividends

one of the most well-known REITs in the market

Focused breakdown of Simon Property Group—one of the most well-known REITs in the market.

Overview

Simon Property Group (SPG) is the largest re ...

Subscribe easy2invest.org

Make your money work for you. Articles, videos, shorts, ebooks, books, forum, community and more.

You can cancel anytime.

Log In

Subscribe now

All information in this article is not a recommendation.

We show examples, and you need to analyze.

We are not responsible for your decisions and investments.

Related articles

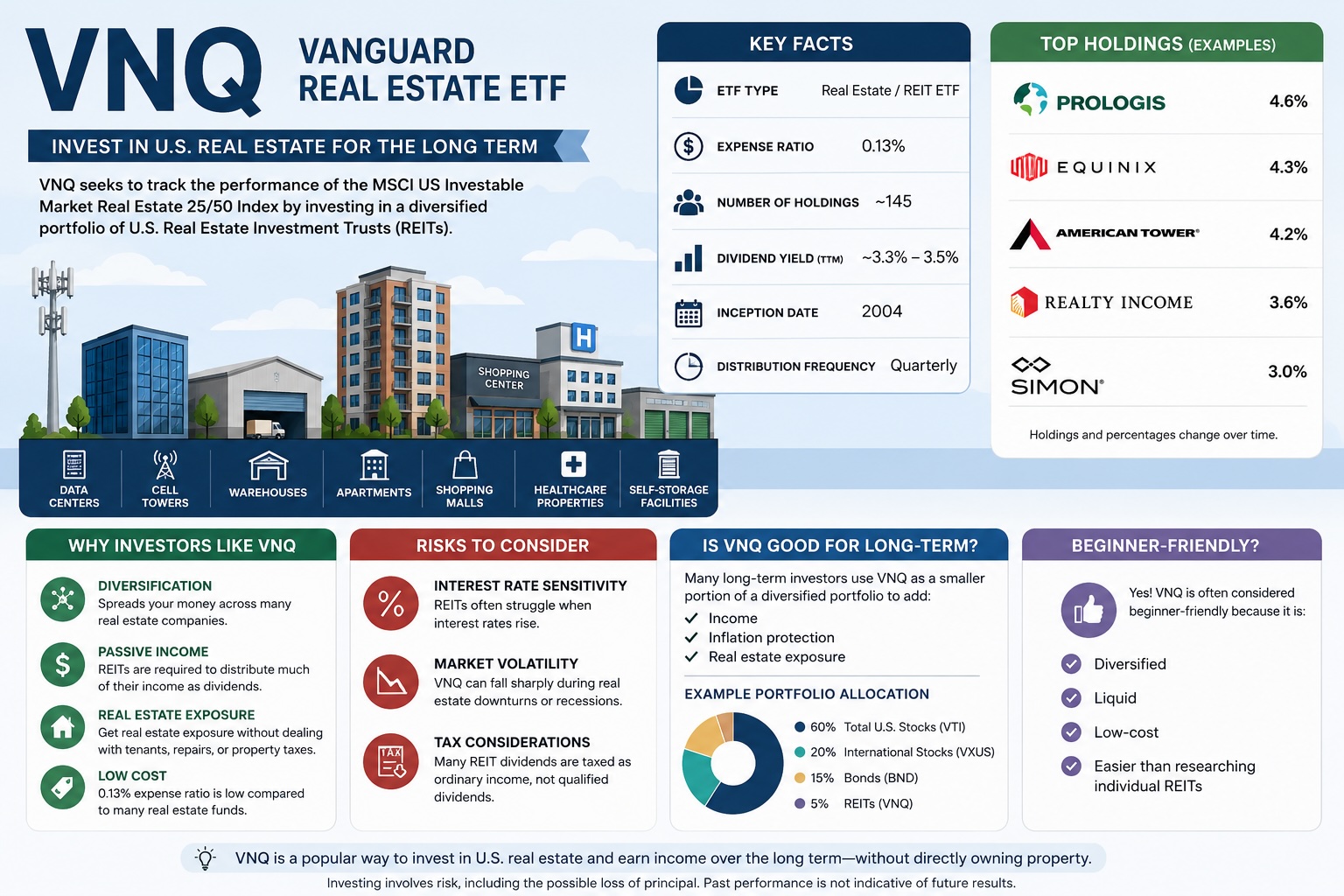

REIT VNQ

VNQ is one of the most popular REIT ETFs for inves

How to buy 15,500 properties without a down payment and receive 5% rent?

This is not clickbait.

What is REIT?

Real Estate Investment Trust

REIT WellTower

One of the most important healthcare REITS

REIT Digital Realty Trust (DRL)

the most important REITs in the digital infrastruc

REIT Equinix for Data-Center (EQIX)

One more REIT to analyze about it

REIT Welltower (WELL)

Welltower (NYSE: WELL) is one of the largest

Prologis (NYSE: PLD) One of the Most Important REITs in the World

Is it a good REIT?

Let's talk about the REIT O

What is Reit O?